Suppliers and the demands of the digital economy: A powerful case for commercial card acceptance

May 5, 2025 | By Sébastien Delasnerie and Jennifer Marriner

Until recently, business-to-business payments hadn’t changed much — dominated by bank or wire transfers and paper checks, they were slow, inefficient and prone to error. Now more financial decision-makers are realizing that the value of digital payments, including cards, extends far beyond the transaction itself, from streamlining reconciliation to optimizing working capital to improving transparency to reducing fraud.

Yet some suppliers remain hesitant to accept cards, still clinging to analog methods in a digital economy. We wanted to know why they’re holding back — and whether those who now accept cards are realizing the benefits of card acceptance — so we launched a global survey of more than 1,000 senior financial executives at large B2B suppliers. And the answers may surprise you.

First, suppliers that do not accept cards say they are concerned about the need for security and fraud prevention. However, in the survey, 31% of businesses that accept cards said they saw increased transaction security. A quarter said they benefited from lower fraud incidence.

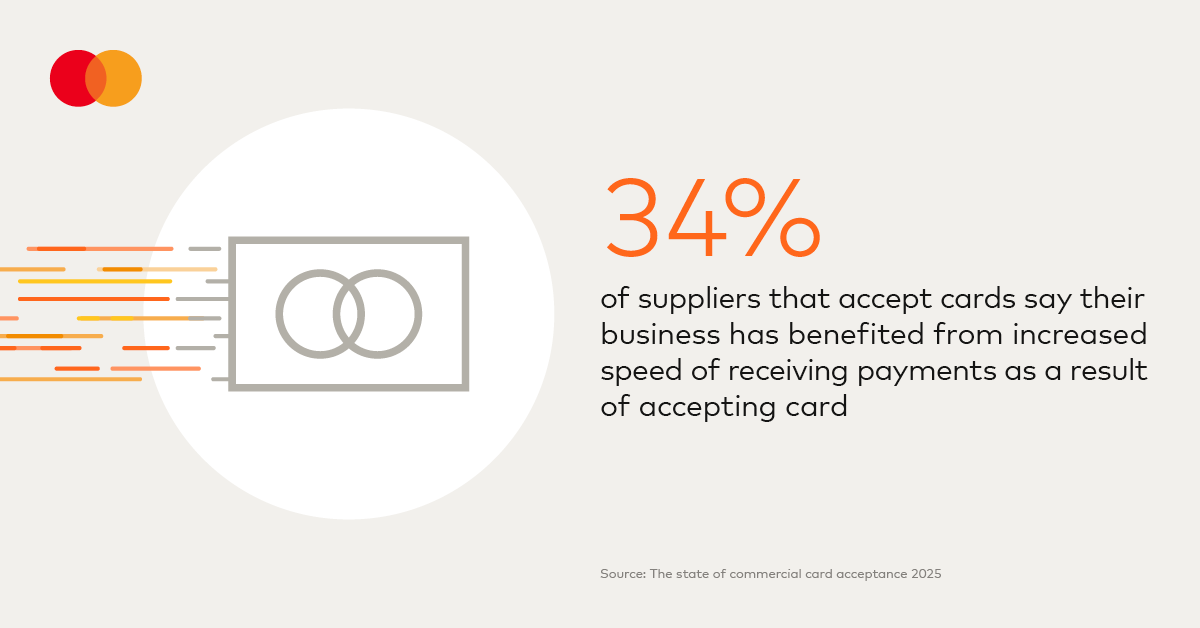

Second, those that didn’t accept cards also worried that integrating card payments with existing operational systems would be too complex. Yet accepting cards can reduce the complexity elsewhere in their businesses, as non-card payments don’t come with the same rich data that speeds up tedious accounting. And about 34% of suppliers that have embraced digital payments say their business has benefited from faster receipt of funds because they accept cards.

But that’s not all. Suppliers can also improve overall satisfaction among buyers by offering payment methods preferred by them, such as cards. Of those businesses surveyed that do accept cards, a third said that they’ve been able to improve customer convenience as a result.

Working capital is key to financial health, giving businesses the liquidity, flexibility, and resilience to meet short-term obligations, pursue growth, and withstand economic challenges with confidence. And it’s a significant pain point for 71% of suppliers surveyed. The research revealed that businesses that accept cards are 14 percentage points more likely to say that their businesses are very efficient at maximizing working capital than those that don’t.

Suppliers that accept cards also report increased operational efficiencies, listing greater payment visibility, faster processing speeds and lower payment-processing costs as their top benefits.

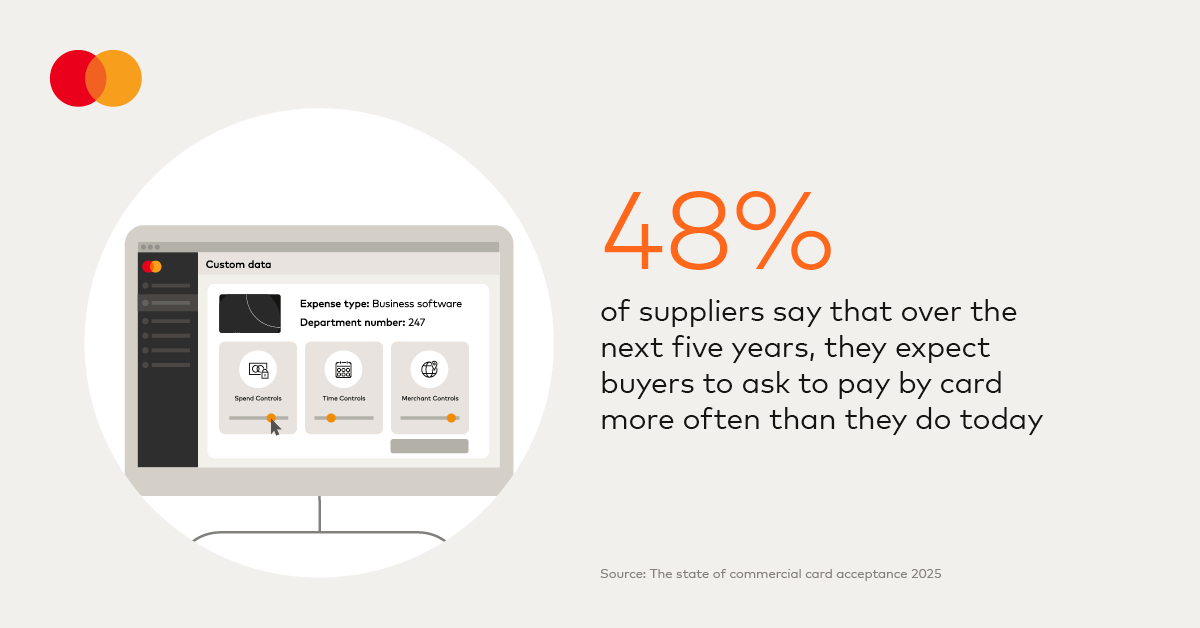

Card acceptance isn’t a silver bullet for suppliers. But it is a valuable option for managing working capital or growing revenue, especially as buyer demand is expected to grow. Nearly half of all suppliers said that over the next five years, they expect buyers to ask to pay by card more often than they do today, according to the survey. But we’re not approaching the boom in commercial card payments as simply inevitable. Rather, we consider it a call for continued innovation. Today, we're creating and delivering new capabilities that fulfill the promise of digitization for buyers and suppliers alike.

After all, buyers are people too: They’ve come to expect straightforward, streamlined payments in their everyday lives. One way Mastercard addresses these buyer needs is through virtual card solutions — payment options that link to an account with an established line of credit and that function just like a regular credit card but come with enriched data and custom controls. And because of their digital nature, they are easily integrated into the software, such as expense management and accounting programs, that businesses rely on.

Ultimately, card acceptance isn’t just about the card — it’s about the data and insights that come along with it, which eases reconciliation, creates more transparency and offers greater insights in real time, allowing businesses to function more efficiently. Mastercard can help suppliers realize these benefits.

Take straight-through processing. Traditional B2B payment processing relies heavily on manual entry, which is rife with challenges, from slow processing times, leading to poor cash flow visibility to human errors that could jeopardize business relationships. With straight-through processing for virtual card numbers, the processing request for the supplier is automated and delivers approved funds straight to the supplier’s bank account, no manual intervention required. Mastercard Receivables Manager does just that, facilitating the delivery of remittance data directly to enterprise resource planning or accounting systems.

The potential of these benefits can be supercharged with the application of artificial intelligence and machine learning tools for ever faster reconciliation and more data transparency.

Suppliers accepting cards today are leaning into AI, with more than a third using it to forecast their cash positions, boost security and increase transaction speed. And 96% would like AI to make recommendations to improve the efficiency of payment processes, and the top capability for businesses seeking a new payment provider is AI-powered tools.

We can’t deliver these benefits on our own. Our innovation springs from collaboration with acquiring banks and business platforms to improve the overall experience — creating spaces to test out ideas and experiment with new ways to drive B2B payment experiences that are equally frictionless and secure. As our research shows, companies that embrace cards can manage their challenges better and create new efficiencies and opportunities, unlocking the potential that ultimately strengthens the digital economy for everyone.

Sébastien Delasnerie is executive vice president for Corporate Solutions at Mastercard. Jennifer Marriner is executive vice president for Acceptance Solutions at Mastercard.

White paper

Breaking down barriers in commercial card acceptance

Innovation in commercial payments can create new opportunities around optimization, visibility and efficiency for suppliers, which will lead to revenue and growth opportunities.

Download the report

White paper

The state of commercial card acceptance 2025

A new global survey of more than 1,000 senior financial decision-makers at large B2B companies shows how accepting cards improves cash flow and processing inefficiencies, and dives into the potential for automation and AI to simplify payments and streamline operations.

Download the report

Newsroom

Newsroom