‘I didn’t buy that … did I?’: Helping shoppers solve the mystery of ‘friendly fraud’

June 10, 2020 | By Brendan CoffeyReviewing a credit card bill can sometimes feel like a walk down memory lane. Certain charges recall takeout from a favorite restaurant or the arrival of a hotly anticipated online purchase. But occasionally, some charges don’t look familiar at all. A meal at a national fast-food chain might actually have been billed by the franchise that runs the location. Gas stations may route pump charges through a payment provider in another state, or a web retailer could be owned by an individual with a different name.

As online commerce grows, friendly fraud has been on the rise. More than 1 in 7 consumers have mistakenly disputed a legitimate transaction, according to a new Aite Group survey of 1,004 U.S. consumers commissioned by Ethoca, a Mastercard company that provides collaboration-based intelligence and technology solutions that fight fraud, prevent disputes and improve the customer experience.

That high level of voluntary disclosure by cardholders means that an industry-estimate 15% to 20% of disputes result from friendly fraud is probably low. In specific categories, such as subscriptions and digital goods like e-books and online games, merchants interviewed by Aite contend that upwards of 75% of all their disputes are friendly fraud.

“The research validates what we've been hearing from card issuers and merchants for some time — that false claims from confusing or scant transaction information are creating a poor customer experience," says Keith Briscoe, Ethoca’s chief marketing and product officer.

In any case, the costs add up. Aite Group says the formal dispute process called chargebacks, of which friendly fraud is a significant part, costs banks $690 million annually, and they expect that number to climb to $1 billion by 2023. Total administrative costs can be as high as $75 per dispute.

Then there’s the cost to consumers. About 75% of credit card users and 83% of debit card users spend time researching a charge before disputing it. Even so, about 27% of consumer calls to dispute a charge end up with them realizing they made the purchase.

Beyond the time and effort lost, unrecognized friendly fraud feeds misinformation into the complex transactional models used by issuers, so more transactions get flagged as potential fraud and consumers risk experiencing false declines when they try to use their card, increasing frustration.

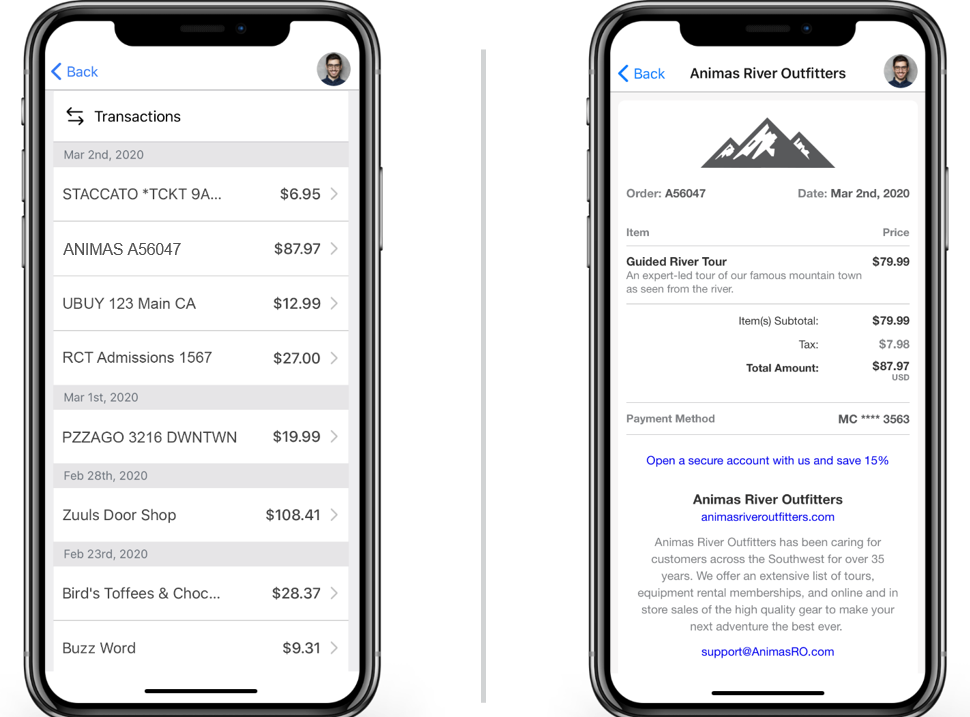

One way to solve the problem is by providing consumers with quicker, fuller information about their transactions. Ethoca’s Digital Receipts service enables banks to provide consumers with a detailed electronic receipt from participating merchants through the banks’ mobile or desktop app. By providing consumers with more information about a transaction that confuses them, it can help them identify a charge they forgot, avoid the time and cost of a phone call to customer service and ultimately reduce friendly fraud and the longer-term ramifications on retailers and consumers.

In a recent expansion of the service, Ethoca announced a deal in April with Microsoft, which will provide participating banks with detailed transaction information on all Microsoft products — so if a customer is questioning the Microsoft purchase, they can access the receipt immediately on their bank’s app, with much more detailed information — a clear merchant description, the merchant’s logo, full product description and more. This eliminates the need for unnecessary disputes and chargebacks.

According to the Aite survey, more than 80% of consumers say they regularly retain their paper receipts in large part to try and reconcile with their statements. Fully 89% of consumers say that a picture of the receipt would have been helpful in heading off disputes over charges they didn’t recognize. Ethoca is betting that giving consumers the receipt digitally will slash the time, frustration and costs everyone suffers from friendly fraud. The service, which debuted last year, is already in use by a top five (by assets) U.S. bank.

Results from existing Ethoca collaborations show that consumer inquiries about seemingly unfamiliar charges drop by 15% to 30% when they have immediate access to the digital receipt through a channel they trust. That in turn slashes costs to merchants and banks and delivers consumers a better experience — a walk down memory lane, but this time with directions.

Newsroom

Newsroom