Jamaica’s Journey to Financial Inclusion: What's Needed to Unlock the Next Growth Phase

May 26, 2026 | Kingston, JamaicaNew research shows that while financial access and traditional banking usage are strong, merchant acceptance gaps prevent digital payments from becoming the everyday norm despite strong consumer trust and demand.

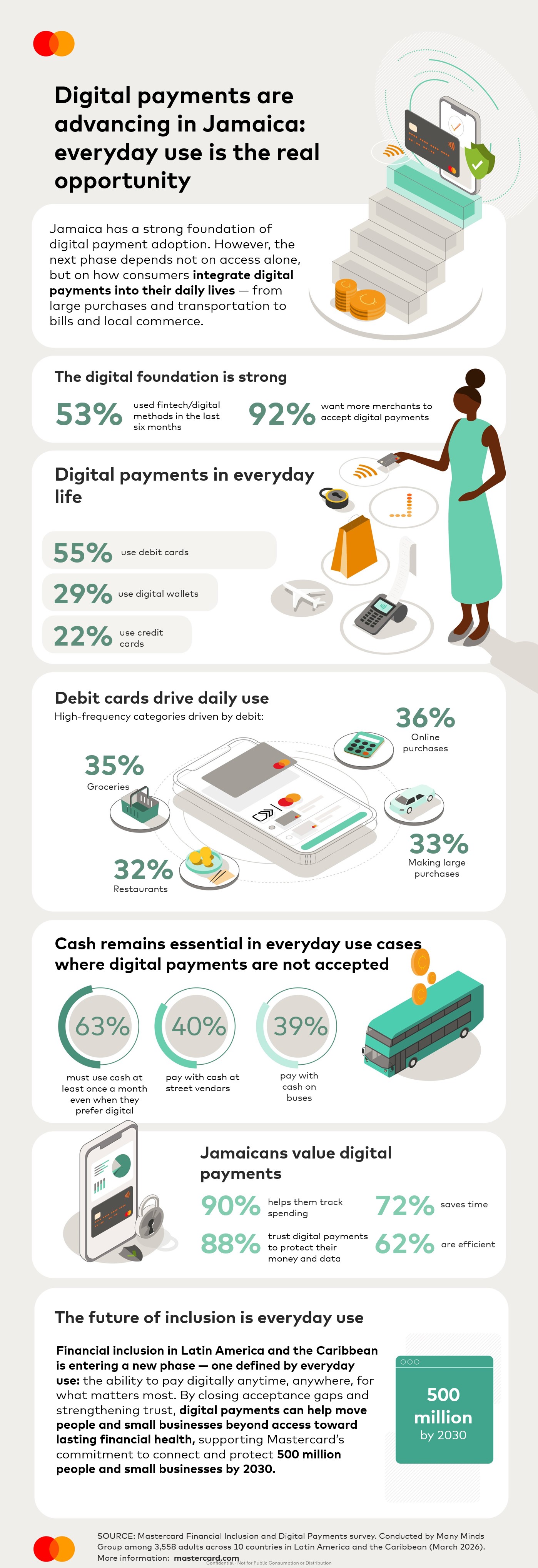

A new Mastercard study on the State of Digitalisation and Financial Inclusion in Jamaica shows a strong foundation for wider digital payments but faces critical merchant acceptance barriers. According to the World Bank, Global Findex 2021, 73.3% of Jamaicans are banked. Yet despite this foundation, and strong consumer trust in digital payments, the country remains significantly cash-dependent due to these merchant infrastructure gaps with 92% of Jamaicans wishing more stores would accept digital payments.

The opportunity now lies in enabling consistent everyday digital payment usage by expanding merchant acceptance networks through daily transactions—from groceries and transportation to recurring bills.

The Infrastructure Gap: Trust Exists, but Barriers Remain

The study suggests that Jamaicans demonstrate strong knowledge of traditional banking tools and express high confidence in digital payment security.

Traditional banking knowledge is high:

- 87% with debit cards

- 85% with bank savings accounts

- 78% with remittance services

- 64% with digital wallets

But when it comes to newer emerging payment methods, there’s a severe lack of knowledge:

- 80% with payroll cards

- 79% with BNPL (Buy Now Pay Later) services

- 76% with cryptocurrency wallets

When deciding which payment method to actually use, trust (94%), understanding (92%), and security (91%) rank as the top three most important factors.

However, knowledge of how a tool works is necessary but not enough. Jamaicans won't adopt a payment method, even if they're aware of it, until they understand how it works, trust the institution, and feel secure using it. This explains why debit leads while emerging solutions lag (knowledge gaps create trust gaps). Adoption follows confidence, not awareness which is evident in Jamaicans payment behavior.

"Jamaicans are deeply familiar with traditional banking—debit cards, savings accounts, remittances—because they've built trust through understanding and consistent use. But when something is new, that familiarity disappears. We see it with emerging solutions like BNPL or cryptocurrency – high unawareness, lower adoption,” said Dalton Fowles, Country Manager, Mastercard Jamaica. “The lesson is clear: trust follows understanding. If we want broader digital adoption, we can't just introduce new tools. We need to build understanding alongside them, so consumers can develop the confidence to use them the way they've learned to use debit.”

Debit Dominance: How Understanding Drives Usage

For Jamaican consumers, debit has emerged as the dominant and most trusted everyday payment tool. 55% of Jamaicans actively use debit cards, with usage patterns revealing clear preference for this method across all major transaction categories:

- Debit-led transactions: online purchases (36%), groceries (35%), restaurants (32%)

- Cash-dependent transaction: street vendors (40%), buses (39%), rent (27%)

However, credit card adoption remains exceptionally low at only 22%, signaling that Jamaicans prefer a spend-what-you-have approach over borrowing, reflecting a financially conservative and fiscally responsible mindset.

This pattern is clear: Jamaicans use what they understand and trust. When merchant infrastructure expands to support these preferred methods, particularly debit and digital wallets, universal adoption will be achieved. In Jamaica, that infrastructure expansion hasn't materialized yet, creating a critical gap between consumer readiness and merchant capability. Only 8% of small merchants in Jamaica have a point-of-sale solution to accept digital payments, with just 11 POS terminals per 1,000 inhabitants. This explains why cash remains stubbornly dominant, accounting for approximately 72% of personal consumption payment volume across the island. Meanwhile, contactless penetration stands at 56%, illustrating strong adoption among those who can use it, but is also a signal that most merchants haven't yet enabled the option.

Mastercard's Commitment: Building the Infrastructure and Confidence Jamaicans Need

Closing this merchant acceptance gap is essential to Jamaica's digital economy. This moment represents an opportunity to expand merchant networks while delivering the trusted, frictionless payment experiences that consumers demand.

Through proven solutions like Contactless, Tap on Phone, and Click to Pay, combined with targeted merchant and consumer education initiatives, Mastercard is working with financial institutions, merchants, and government stakeholders to build the seamless digital ecosystem Jamaicans need and want. These solutions enable merchants of all sizes to accept digital payments easily and securely.

"Jamaica's financial confidence is outstanding," said Fowles. "What's needed now is coordinated action, building the merchant networks where Jamaicans shop daily, while ensuring they have the knowledge and confidence to use digital options reliably. As Jamaica advances toward a more fully digital economy, the future of financial inclusion will depend on how easily people can pay for the things that matter most in their daily lives, wherever they are."

Media Contacts

Methodology

The study was led by Mastercard conducted by the independent research Many Minds Groups. Data referenced in this report comes from a survey of n=217 adults aged 18 years and older in Jamaica, part of a larger survey across 10 countries in the region conducted by Mastercard. The survey was conducted from February 11-23, 2026. The margin of error for Jamaica data is ±5% at the 95% confidence level. Note, sub-group analysis should be interpreted directionally as bases are less than n=100 (these audiences are marked with an asterisk).

About Mastercard

Mastercard powers economies and empowers people in 200+ countries and territories worldwide. Together with our customers, we’re building a sustainable economy where everyone can prosper. We support a wide range of digital payments choices, making transactions safe, simple, smart and accessible. Our technology and innovation, partnerships and networks combine to deliver a unique set of products and services that help people, businesses and governments realize their greatest potential.