Northeast Asia Economic Update: Winning ASEAN Visitors in Hong Kong

April 23, 2026 | Wei LI, Economist from Mastercard Economic InstituteAs Hong Kong's inbound tourism recovery continues to gain momentum, one segment is quietly rewriting the story of who's coming — and how much they're spending. ASEAN visitors are emerging as a fast-growing and increasingly high-value force, playing a pivotal role in diversifying demand beyond Chinese Mainland travelers.

In this post, we dig into the latest data on ASEAN tourists in Hong Kong. We look at why inbound tourist growth accelerated further in Q1 2026, what scheduled flight data tells us about the summer peak ahead, and how the overall visitor mix by travel duration is holding steady. Most importantly, we explore why ASEAN visitors stand out as a resilient and high-spending segment — and what their more balanced, experience-led spending profile means for Hong Kong's tourism economy.

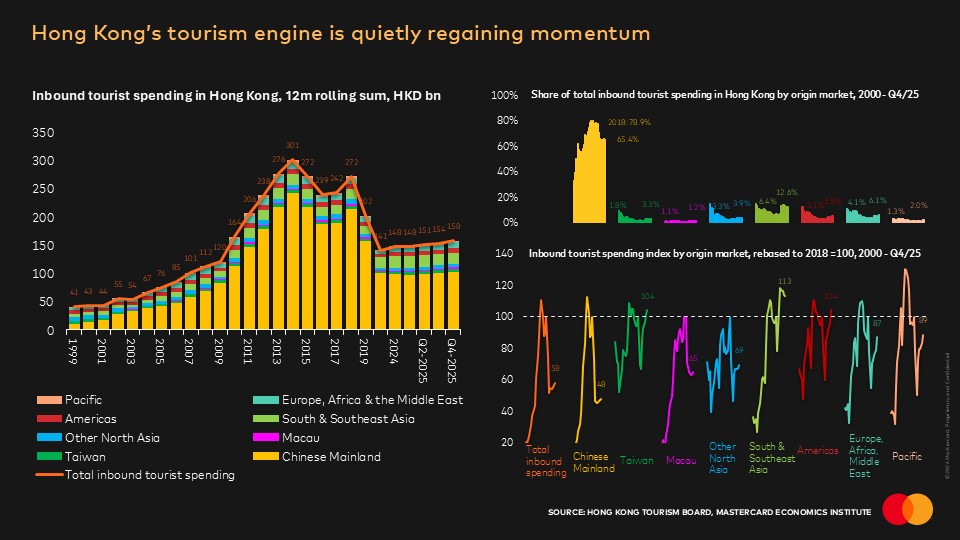

1. Hong Kong’s tourism engine is quietly regaining momentum, and increasingly being powered by a broader mix of visitors. Inbound tourism revenues have continued their gradual recovery, reaching around HKD 158bn in 2025, and shifting from a drag on growth in 2024 to a meaningful tailwind—contributing around 0.7ppt to GDP growth. While Chinese Mainland visitors remain the cornerstone (~65%+ of total spending, vs. ~79% in 2018), the composition of demand has been evolving. Southeast Asian markets now account for roughly 13% of total inbound spending (up from ~6% in 2018), with spending recovering to around 113 (2018=100) as of Q4-2025—one of the strongest performances across regions. This outperformance reflects a combination of rising incomes, improved connectivity, and a shift toward more experience-led travel.

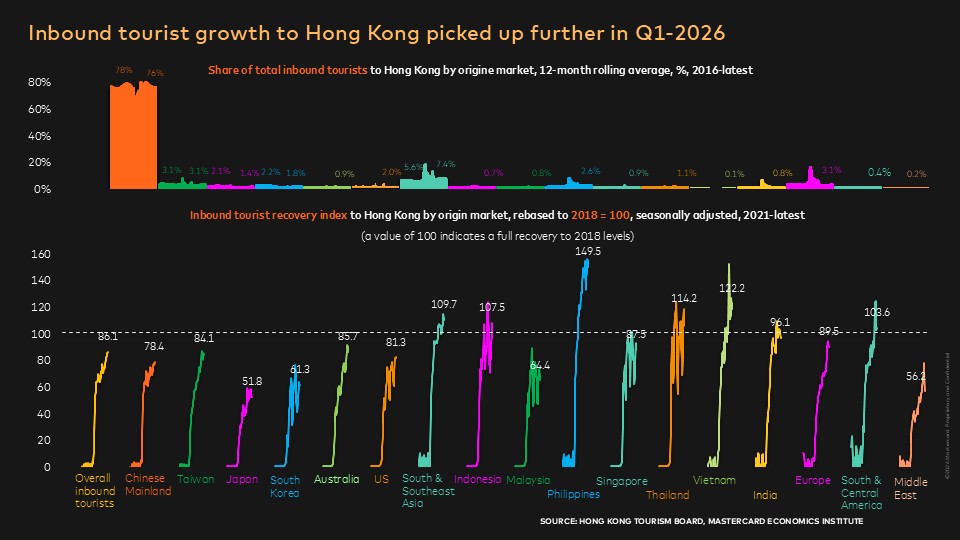

2. Inbound tourist growth to Hong Kong picked up further in Q1-2026, totalling 14.3mn arrivals (+17% y/y), compared with 12% growth in 2025. Our calculations suggest this acceleration is increasingly driven by ASEAN markets. In particular, arrivals from the Philippines (~150% of 2018 levels), Vietnam (~122%+) and Thailand (~114%+) are leading the rebound, while Singapore and Indonesia are also approaching or exceeding pre-pandemic levels. Beyond ASEAN, arrivals from South and Central America have also surpassed 2018 levels, underscoring Hong Kong’s evolving role—not just as a tourism hub, but as a key connector between China and the Global South. This trend is likely benefiting from China’s accelerating outbound investment (ODI) and growing B2B travel flows, which are supporting demand beyond traditional leisure segments.

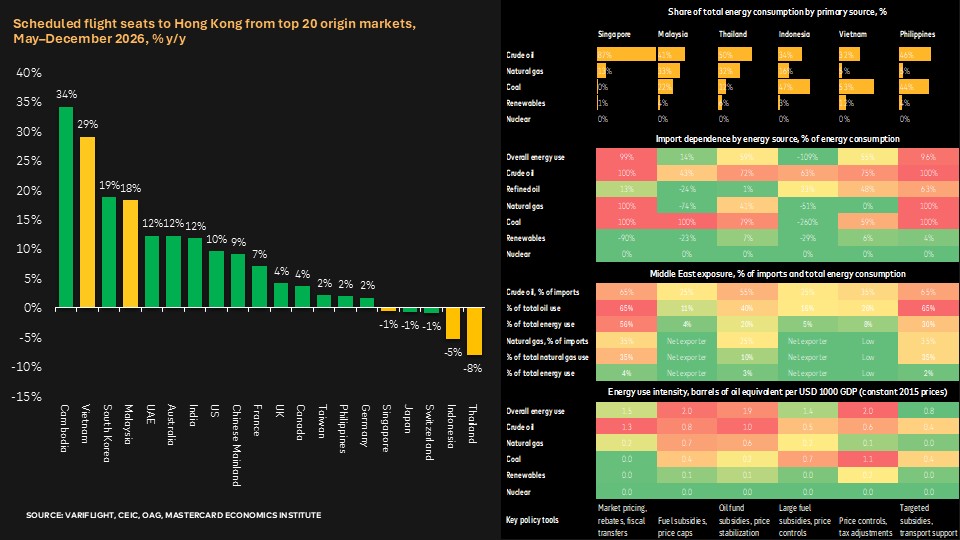

3. Looking ahead to summer peak season, scheduled flight data points to continued strengthening in inbound travel to Hong Kong, with seat capacity from Vietnam (+29% y/y) and Malaysia (+18%) among the fastest-growing. Other markets, including Cambodia (+34%) and South Korea (+19%), also stand out. However, Indonesia and Thailand lag slightly, with capacity still below last year’s levels. We think this divergence partly reflects the uneven impact of recent energy shocks linked to Middle East tensions. Markets with lower energy intensity and stronger policy buffers appear better positioned to sustain outbound travel demand, alongside improved flight frequencies and firmer economic momentum. Overall, the pipeline of scheduled flights suggests that inbound growth to Hong Kong is likely to remain robust into the summer, supporting a more diversified and resilient tourism recovery.

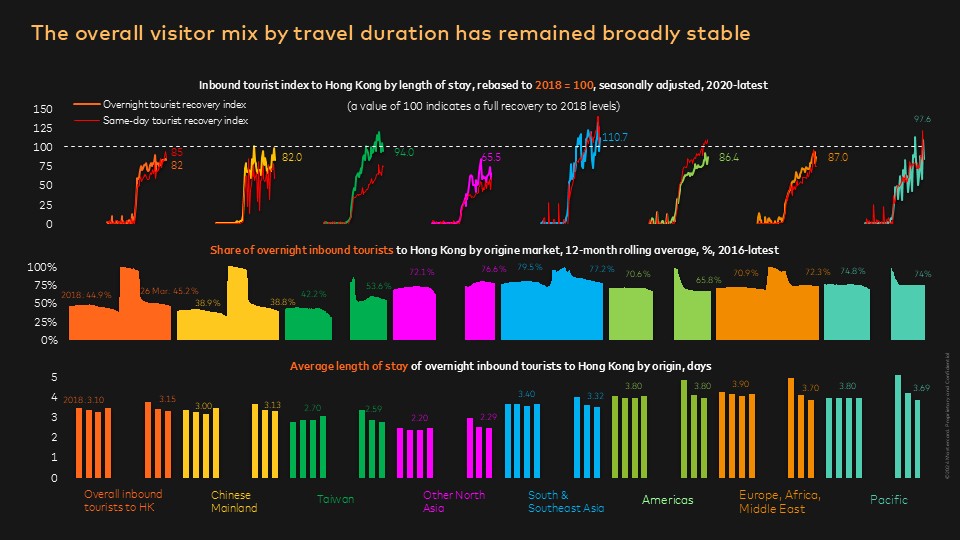

4. The overall visitor mix by length of stay has remained broadly stable. While growth in same-day inbound tourists to Hong Kong has outpaced that of overnight visitors—particularly for ASEAN markets and the Americas—the composition has not shifted materially. The share of overnight visitors stood at 45.2% in March 2026, broadly in line with 44.9% in 2018, suggesting that the recovery has not diluted stay-duration dynamics. Visitors from South and Southeast Asia continue to exhibit relatively stable travel duration, averaging around 3.3–3.4 days, largely unchanged from 2018. At the same time, the rising share of same-day trips points to the growing importance of short, flexible travel patterns, likely supported by improved connectivity and the option to base themselves in nearby Chinese Mainland cities where accommodation is more economical. In contrast, travellers from the Americas and the Pacific have seen a more noticeable shortening in length of stay.

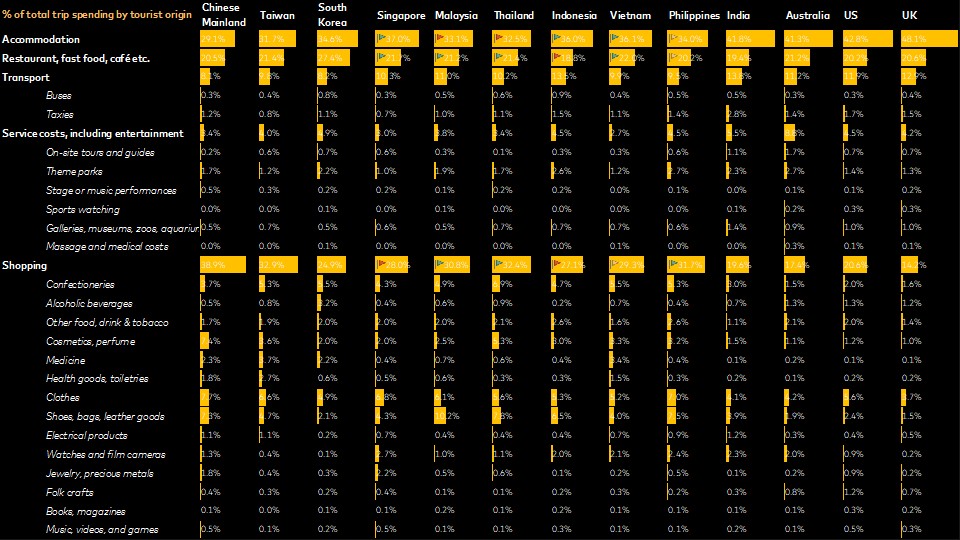

5. In terms of spending per tourist in Hong Kong, ASEAN markets continue to stand out as a resilient and increasingly important source of value. Visitors from South and Southeast Asia are now spending around HKD 5,200–5,300 per trip on average, exceeding pre-pandemic levels, supported by improving economic conditions and sustained inflation in source markets. This contrasts with the trend among Chinese Mainland tourists, in which spending patterns have shifted away from shopping-led travel, with a lower share of high-ticket discretionary purchases such as luxury goods, cosmetics, and electronics in Hong Kong. This reflects a combination of greater price sensitivity, increased domestic availability of goods, and a broader shift toward experience-led consumption rather than retail arbitrage.

6. In terms of spending patterns, surveys show that ASEAN visitors exhibit a more balanced and experience-led consumption profile compared with other markets. While shopping remains important, its share is generally lower than that of Chinese Mainland visitors (around 27–32% vs. ~39%), with a relatively higher allocation toward accommodation (low-30s%) and dining (around 20–22%). Within ASEAN, there is notable variation. The Philippines, Thailand, and Malaysia show relatively higher spending on shopping (often above 30%), while Singapore, Indonesia, and Vietnam allocate more toward accommodation and services. In particular, Indonesia and the Philippines exhibit a slightly higher share of spending on services and experiences—including entertainment and attractions—compared with the ASEAN average.

###